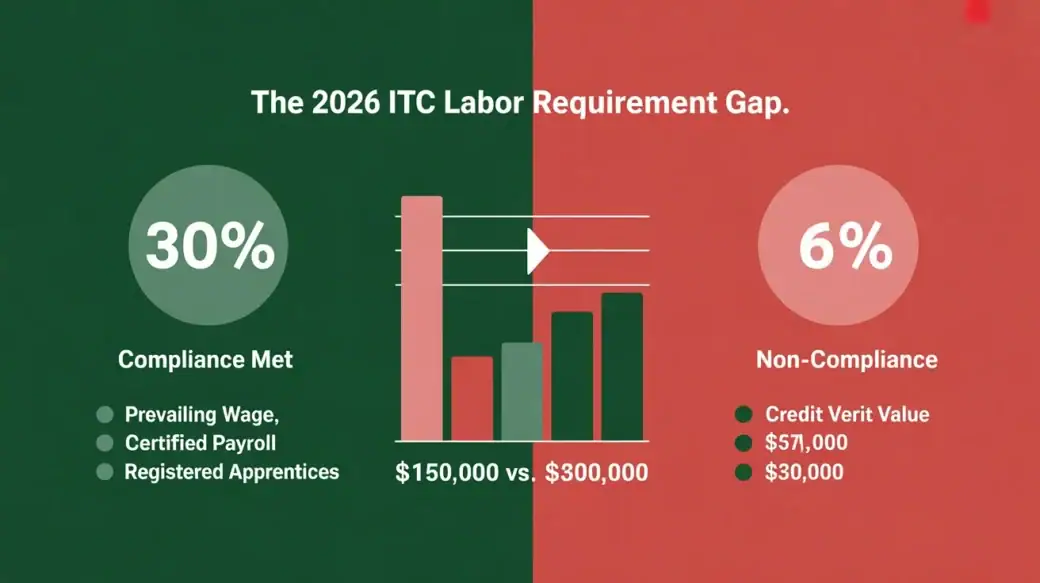

The IRS Section 48 energy credit is a federal Investment Tax Credit that lets businesses cut their tax bill by 30% of qualified solar system costs in 2026. According to SolarInfoPath’s review of current IRS guidance, this 30% rate only applies when the installer pays prevailing wages and uses registered apprenticeship workers. Projects that skip those labor rules get only a 6% credit rate. That one difference equals $96,000 on a $400,000 system.

Introduction to the IRS Section 48 Energy Credit

A business signs a solar contract based on a 30% credit projection. The system gets installed. Tax season arrives, and the actual credit is far smaller than expected. This is not a rare situation. It happens because three key conditions must all be true for the full 30% to apply.

Your business must owe enough federal tax to absorb the credit. Your installer must have paid prevailing wages and kept certified payroll records. And the qualified cost basis must exclude roof work and structural costs. If any one of these is missing, the credit shrinks or gets delayed.

This guide covers each of those conditions in plain terms so you know exactly what to expect before you sign anything.

SolarInfoPath Reality Check: The solar ITC is not automatic at 30%. The IRS requires proof of prevailing wage compliance through certified payroll records. Without those records, the credit rate defaults from 30% to 6% under the Inflation Reduction Act rules that took effect for 2023 and later projects. Most installers do not volunteer this detail during the sales process.

What Is the IRS Section 48 Energy Credit?

Section 48 Is a Business Tax Credit, Not a Homeowner Credit

Section 48 of the Internal Revenue Code is a federal investment tax credit for businesses and commercial property owners. It is not available to homeowners. Homeowners use Section 25D for residential solar installations.

Section 48 covers commercial solar systems, combined heat and power systems, fuel cells, small wind turbines, and standalone battery storage systems added under the Inflation Reduction Act of 2022.

A Tax Credit Saves More Money Than a Tax Deduction

A tax credit cuts your actual tax bill dollar for dollar. A tax deduction only reduces the income that gets taxed. For a business in the 21% corporate tax bracket, a $300,000 deduction saves about $63,000 in taxes. A $300,000 tax credit saves the full $300,000.

This is exactly why the solar investment tax credit is worth understanding carefully before you go solar commercially.

What Does Section 48 Cover for Solar

Section 48 covers these specific costs when you install a commercial solar system:

- Solar panels and photovoltaic modules

- Inverters, including string inverters, microinverters, and power optimizers

- Mounting hardware and racking systems attached to the structure

- Wiring and conduit that are directly part of the solar system

- Monitoring systems that are built into the solar setup

- Battery storage placed near or directly connected to the solar array under IRC Section 48(c)(6)

- Installation and labor costs are tied directly to the qualifying solar equipment

The ITC percentage is applied to the total of these specific costs. That total is called your qualified basis.

How the Solar Investment Tax Credit (ITC) Works

The ITC Lowers Your Tax Bill Directly, but cannot create a Refund

The ITC is a nonrefundable tax credit. It reduces the tax you owe the IRS to zero, but it cannot go below zero. It will not create a refund check.

A business installs a $500,000 solar system and earns a $150,000 ITC at 30%. If that business only owes $100,000 in federal taxes that year, only $100,000 of the credit is used. The leftover $50,000 is not lost. It carries forward under Section 39 rules.

Unused ITC Carries Back One Year or Forward Up to 20 Years

Section 39 of the Internal Revenue Code gives businesses two options for unused ITC. They can carry it back one prior tax year by filing an amended return. They can also carry it forward for up to 20 future tax years.

The carryback option is useful if your prior year had a larger tax bill than the current year. Many commercial buyers do not know this option exists. They assume unused credit is simply wasted.

The Solar ITC 2026 Rate Is 30% Only With Prevailing Wage Compliance

For commercial solar systems placed in service in 2026, the base credit rate is 30%. That rate requires the installer to pay prevailing wages as defined by the Davis-Bacon Act throughout the entire construction period.

Systems that do not meet the prevailing wage and registered apprenticeship rules get a 6% credit rate instead of 30%. On a $400,000 installation, that difference equals $96,000. That single compliance gap is enough to change whether commercial solar is financially worth it for your business.

What Costs and Systems Qualify Under Section 48

Qualified Equipment Is Specifically Defined by the IRS

The IRS allows these items as qualified costs for the Section 48 ITC:

- Solar photovoltaic panels and modules

- Inverters of all types, including string, micro, and power optimizer models

- Mounting and racking hardware that holds the panels in place

- Wiring and conduit that are part of the solar energy system

- Monitoring systems that are integrated into the solar installation

- Battery storage placed next to or connected to the solar array per IRS Notice 2023-29

- Direct installation and labor costs for the qualifying equipment listed above

These costs form your qualified basis. The ITC rate is multiplied by this number to get your credit amount.

The IRS Excludes These Costs From the ITC Basis

These items appear on many solar invoices but do not qualify for the ITC:

- Roof repairs or full roof replacements, even when done right before panel installation

- Electrical panel upgrades that serve the building and not just the solar system

- Landscaping or grading that is not needed for the solar equipment itself

- Financing charges and loan interest on the solar project

- Permit and inspection fees in most cases

Including any of these in your credit calculation overstates the qualified basis and creates direct audit exposure with the IRS.

SolarInfoPath Reality Check: Installers Include Roof Costs That Do Not Qualify

SolarInfoPath’s review of 2026 commercial solar contracts shows that installers frequently bundle roof repair costs into the total project price. They then present that full amount as the ITC basis.

The IRS and the U.S. Tax Court have consistently rejected structural costs from the ITC basis. These costs serve the building, not the solar system. Before signing any contract, ask for an itemized invoice that separates solar costs from structural work. Have your tax professional confirm which line items qualify.

Eligibility Requirements for the Section 48 Tax Credit

You Must Own the Solar System to Claim Section 48

The Section 48 credit belongs to the system owner. If your business signs a solar lease or a power purchase agreement, a third party owns the system. You cannot claim the ITC on equipment you do not own.

In lease and PPA deals, the solar company keeps the credit. They may reflect part of that value in a lower energy rate for you. But your business does not file for any ITC. For more on how this works in practice, understanding solar power purchase agreements and what they actually deliver is important before you sign.

IRS Section 469 Passive Activity Rules Limit Credits for Some Investors

Passive investors in solar projects face a specific problem. The IRS passive activity rules under Section 469 prevent passive credits from being used to offset active income.

This limitation affects real estate investors and limited partnership structures most often. A manufacturing company or retail business with active operating income generally does not face this issue. But if you are investing in solar as a passive activity, confirm with your tax advisor whether Section 469 limits how and when you can use the credit.

Businesses Eligible for Solar ITC Under Section 48

These commercial structures can qualify for the Section 48 credit if they own a qualifying solar system:

- C corporations that own and operate commercial buildings

- Partnerships and LLCs that use the system in an active trade or business

- S corporations that pass the credit through to owners on Schedule K-1

- Sole proprietors with qualified business income and a qualifying solar system

- Agricultural businesses using solar on working farm or ranch land

- Tax equity investors who fund solar projects specifically to absorb ITC and depreciation benefits

For a detailed look at how tax equity arrangements work, how solar tax equity partnerships are structured, and explains the mechanics and what each party receives.

Understanding Solar ITC Rates and Potential Value

The 2026 Solar Tax Credit Percentage Is 30% With a Possible 40% or 50% Total

The base ITC rate for 2026 is 30% for systems meeting prevailing wage and registered apprenticeship rules. Three separate bonus credits can add 10% to 20% more on top of that base rate.

Reaching 50% total requires meeting all three bonus categories at once, which is uncommon in practice. But the 40% rate with the Energy Community Bonus is achievable for many commercial projects in eligible areas.

Three Bonus Credits That Can Raise Your Total ITC Above 30%

Each bonus credit has a specific qualifying condition. Here is what each one requires and how much it adds:

- Energy Community Bonus adds 10%: Your system must be in an area affected by coal plant or coal mine closures, or on a brownfield site as defined in IRS guidance published under the Inflation Reduction Act

- Domestic Content Bonus adds 10%: Your system must use steel, iron, and manufactured components produced in the United States at the thresholds defined in IRS Notice 2023-29

- Low Income Community Bonus adds 10% to 20%: Your system must be in a qualifying low-income census tract and receive an annual capacity allocation from the IRS

Each bonus requires separate documentation. You cannot assume eligibility. Your tax professional must confirm which bonuses your project qualifies for before you file.

How Much ITC Can You Claim: A Real Dollar Calculation

A commercial building owner installs a 150 kW rooftop system. The total qualified cost is $375,000. The property sits in an energy community.

| Credit Part | Rate | Dollar Value |

| Base ITC with prevailing wage compliance | 30% | $112,500 |

| Energy Community Bonus | 10% | $37,500 |

| Total ITC | 40% | $150,000 |

If this business owes $180,000 in federal taxes, the full $150,000 credit is used in year one. If the business only owes $90,000 that year, the remaining $60,000 carries forward to the next tax year under Section 39.

Comparing Section 48 With Other Solar Tax Credits

Section 48 vs Section 25D

Section 48 is for businesses, and Section 25D Is for Homeowners Only

Section 48 applies to commercial solar systems owned by a business or commercial property owner. Section 25D applies only to homeowners who install solar on their primary or secondary residence. These two credits cover completely separate situations.

Section 25D is filed on Form 1040 as a personal credit. Section 48 is filed on Form 3468 as a general business credit. Section 48 also comes with basis reduction rules, passive activity limits, and carry-forward provisions that do not exist under Section 25D.

Splitting the Credit When a Home Is Also a Business

A taxpayer who uses part of their home as a dedicated business space may need to split the solar system cost between Section 25D and Section 48. The percentage of business use determines how much goes to each credit.

This situation requires a tax professional to calculate correctly. Using the wrong section for the wrong portion of the system results in a filing error.

Section 48 vs Section 48E

Section 48E Replaced Section 48 for Projects Starting After December 31, 2024

Section 48E is the Clean Electricity Investment Credit created by the Inflation Reduction Act. It applies to all projects that begin construction after December 31, 2024. The old Section 48 used a fixed list of approved technologies. Section 48E uses a greenhouse gas emissions test instead of a technology list.

For solar projects, the 30% credit rate is the same under both frameworks. The key difference is in how you prove eligibility and what documentation the IRS requires for the credit to hold up.

The Section 48 to Section 48E Transition Rule: Most Articles Skip

IRS Notice 2024-27 explains the transition rules between Section 48 and Section 48E. If your project began construction before January 1, 2025, you may still qualify under the old Section 48 rules by election.

SolarInfoPath Reality Check: If your project began construction in late 2024 but was not placed in service until 2025 or 2026, you need to confirm with your tax advisor which framework applies. Using Section 48 rules on a project that legally falls under Section 48E will produce a credit that the IRS can reject.

How to Claim the Section 48 Tax Credit

You Claim the Section 48 Credit on Form 3468 and Form 3800

Form 3468, Investment Credit, is the IRS form where you calculate your Section 48 solar ITC. That amount then carries to Form 3800, General Business Credit, which handles all business credits together.

If your business is a partnership or S corporation, the credit is calculated at the entity level on Form 3468. It then passes to each owner through Schedule K-1 with the specific credit amount listed.

Four Documents Your Tax Professional Needs to File the ITC Correctly

These records are required to support a Section 48 credit claim on your tax return:

- An itemized invoice from your installer that separates qualified solar costs from roof work, structural costs, and other excluded items

- Proof of the placed in service date, such as a utility permission to operate letter or interconnection approval document from your grid operator

- Certified payroll records from your installer showing that all workers received prevailing wages as required by the Davis-Bacon Act for your project location

- Location verification documents if you are claiming the Energy Community Bonus or the Domestic Content Bonus

Missing any of these documents puts your 30% credit rate at direct risk during an IRS audit.

A System Placed in Service in January Means Your Credit Moves to the Next Tax Year

The ITC is claimed in the year the system is placed in service. Placed in service means fully installed, operational, and ready to produce power. A system finished in December but waiting on grid connection approval in January is legally placed in service in January.

For businesses planning a fourth-quarter credit, this one timing fact can shift the entire credit to the following year. Knowing how interconnection approval timelines work and how long they take before you finalize your year-end tax plan prevents a costly surprise.

Additional Tax Considerations Related to Solar ITC

Unused ITC Goes Back One Year or Forward 20 Years Under Section 39

Section 39 gives you two options when your ITC exceeds your current year tax bill. You can file an amended return for the prior tax year and apply the credit there. Or you can carry the credit forward and use it against future tax bills for up to 20 years.

The carryback option is most useful when the prior year had higher taxable income. Many commercial solar buyers do not know the carryback option exists. It can accelerate the financial benefit without waiting years for the carry-forward to clear.

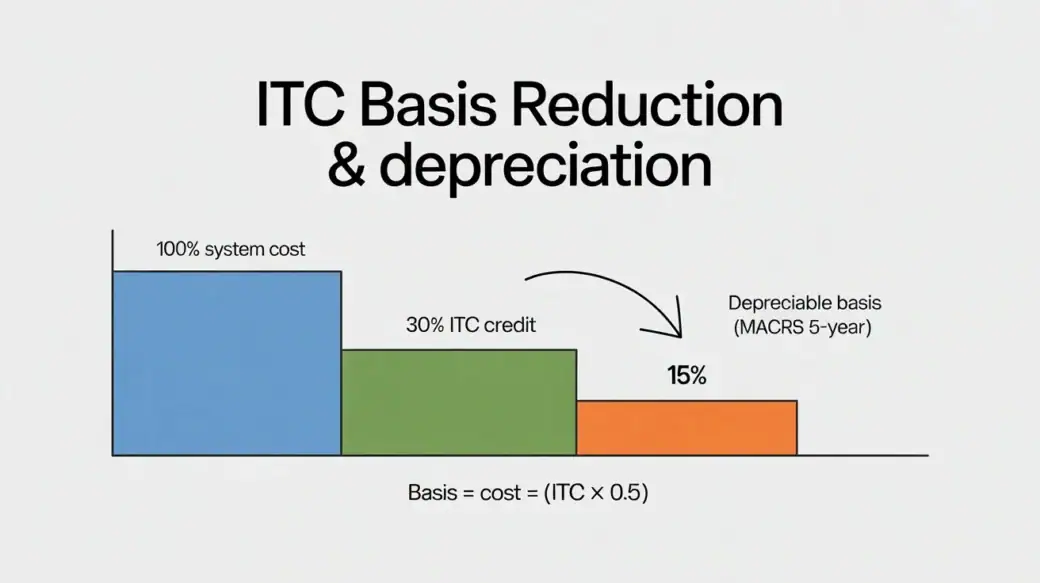

The ITC Basis Reduction Rule Under Section 50(c) Lowers Your Depreciation

When you claim the Section 48 ITC, the IRS requires you to cut your depreciable basis by 50% of the credit amount. This rule comes from Section 50(c) of the Internal Revenue Code.

Here is exactly how it works on a $444,000 system with a $133,200 ITC at 30%. You subtract half the credit, which is $66,600, from the basis. Your depreciable basis becomes $377,400 instead of $444,000. That lower basis means less total depreciation over the life of the system. Skipping this step creates an IRS adjustment that shows up at an audit.

MACRS Depreciation, Solar, and Bonus Depreciation Solar 2026 Work Together With the ITC

Commercial solar systems are classified as 5-year MACRS property. Bonus depreciation for 2025 placed in service property was 40% under the current law before stepping down in later years.

When you take the ITC and MACRS depreciation together, your total first-year tax benefit is larger than either one alone. But the Section 50(c) basis reduction cuts into the depreciation side. A financial model that ignores this step will overstate your total tax savings by thousands of dollars.

Compliance and Key Considerations

Placed in Service Means the System Is Installed and Working, Not Just Contracted

The IRS placed in service standard requires the system to be fully installed, complete, and ready to produce power for its intended use. Signing a contract does not count. Making a payment does not count. Even finishing the physical installation does not count if the utility has not issued permission to operate.

A system that finishes installation in November but does not receive interconnection approval until February is placed in service in February. Your ITC goes on next year’s tax return, not this year’s.

ITC Recapture Applies If You Sell or Remove the System Within Five Years

If your business disposes of the solar system within five years of placing it in service, the IRS will recapture part of the credit you claimed. The recapture amount decreases each year you hold the system.

Here is the exact recapture schedule by year:

- Year 1: The IRS takes back 100% of the credit claimed

- Year 2: The IRS takes back 80% of the credit claimed

- Year 3: The IRS takes back 60% of the credit claimed

- Year 4: The IRS takes back 40% of the credit claimed

- Year 5: The IRS takes back 20% of the credit claimed

A business that sells a commercial building with a solar system in year 2 will owe back 80% of the ITC. This fact rarely appears in commercial solar sales presentations.

SolarInfoPath Reality Check: Prevailing Wage Records Are the Most Common Missing Document

SolarInfoPath’s review of 2026 commercial solar contracts across multiple markets found that certified payroll records are the most frequently missing document in ITC claims. Installers verbally confirm prevailing wage compliance but do not automatically provide certified payroll reports.

The IRS places the burden of proof on the taxpayer, not the installer. If you cannot produce certified payroll records during an audit, the IRS will reduce your credit rate from 30% to 6%. On a $500,000 system, that costs you $120,000 in lost credit after the fact.

Common Mistakes to Avoid

Businesses in a Solar Lease or PPA Cannot Claim the Section 48 ITC

The ITC belongs to the system owner. If you sign a solar lease or PPA, a third party owns the equipment. Your business does not own the system and cannot file for the credit.

Some installers describe the tax credit value as being “passed through” in the form of lower rates. That may describe the economics loosely. It does not mean your business received the ITC. Only the system owner files Form 3468 with the IRS.

Including Roof and Structural Costs in the ITC Basis Triggers Audit Risk

Roof replacement, structural reinforcement, and building electrical upgrades do not qualify for the ITC. These costs help the building. They are not part of the solar energy system under IRS rules.

When these costs appear in the qualified basis, the ITC amount is overstated. If the IRS selects your return for examination, the disqualified costs get removed, and you owe back taxes plus interest. Ask your installer for a line-by-line cost breakdown before any credit is calculated.

Three Filing Errors That Draw IRS Attention on Commercial Solar Returns

These three mistakes appear most often in ITC audit adjustments:

- Skipping the Section 50(c) basis reduction and claiming full depreciation on the pre-credit system cost

- Filing without certified payroll records and claiming the 30% rate instead of the correct 6% rate

- Using a placed in service date that does not match the utility interconnection approval date

Each mistake is fixable before filing. After an audit begins, fixing them costs significantly more in amended returns, interest, and potential penalties.

Example Scenario of a Solar ITC Calculation

A 200 kW Manufacturing Facility System: Full Cost Breakdown

A manufacturing company installs a 200 kW ground mount solar system. The total installer invoice is $480,000. The qualified ITC basis is lower because two cost categories do not qualify.

| Cost Category | Amount | Qualifies for ITC? |

| Solar panels | $240,000 | Yes |

| Inverters and electrical parts | $72,000 | Yes |

| Racking and mounting hardware | $48,000 | Yes |

| Installation labor | $84,000 | Yes |

| Structural foundation reinforcement | $24,000 | No |

| Roof repair before panel installation | $12,000 | No |

| Qualified ITC Basis | $444,000 |

Solar ITC Savings Calculation at 30% and 40%

At 30% with certified prevailing wage compliance, the ITC equals $133,200. The Section 50(c) basis reduction cuts the depreciable basis to $377,400 instead of $444,000.

If this property also qualifies for the Energy Community Bonus, the total rate rises to 40%. The ITC becomes $177,600. The depreciable basis drops to $355,200 after the 50% basis reduction.

What Happens if You Claim the Credit on the Wrong Basis

Using $480,000 instead of $444,000 as the qualified basis overstates the credit by $14,400 at 40%. That may seem small. But if the IRS audits the return and removes the $36,000 in structural and roof costs, the resulting tax adjustment plus accrued interest will exceed $14,400.

Getting the qualified basis right at filing costs nothing. Correcting it after an IRS notice costs significantly more.

Future Outlook for Solar Tax Credits

Section 48E Now Covers All New Projects Started After December 31, 2024

Section 48E is the framework that applies to commercial solar projects beginning construction in 2025 and 2026. It replaced Section 48’s technology list with a greenhouse gas emissions test. The IRA is locked in the credit structure through 2032 with a phase-down beginning in 2033.

This means businesses have a stable planning window through the end of 2032 before any credit reduction takes effect.

The Domestic Content Bonus Requires More Documentation Than Most Projects Expect

The Domestic Content Bonus adds 10% to your ITC rate if your system uses qualifying U.S.-made materials. But the documentation process has proven much harder than the initial IRA guidance suggested.

IRS Notice 2023-29 sets specific material thresholds for steel, iron, and manufactured components. Verifying your supply chain against those thresholds takes additional professional time and cost. Businesses that assumed this bonus was automatic have often found it unavailable after review. Build in an extra documentation budget before claiming this bonus.

IRS Enforcement of IRA Credit Rules Will Increase Through 2032

The ITC structure is stable through 2032. But IRS enforcement of prevailing wage, apprenticeship, and domestic content compliance will get stricter as the agency expands its IRA audit capacity.

For investors watching the commercial solar market, the continued strength of the ITC is one of the main forces driving demand for new installations. This connects to how solar industry demand shapes investment performance across the sector.

What Section 48 Actually Requires and What Most Guides Skip

The ITC Is Conditional on Four Specific Facts, Not One

The ITC is not a flat 30% applied to whatever your installer quotes. Four conditions must all be true for the full credit to apply. Your business must have enough federal tax liability to absorb it. The system cost basis must exclude non-qualifying items. The installer must have certified prevailing wage records. And the system must be placed in service in the correct tax year.

When all four are in place, the ITC significantly improves the financial case for commercial solar and produces a real reduction in your federal tax bill.

When the Real Credit Is Smaller Than the Projected Credit

When any one of those four conditions is not met, the credit shrinks. Low or uneven tax liability delays the benefit across multiple years. An inflated basis that includes roof work gets cut during the audit. Missing wage records reduce the rate from 30% to 6%. A delayed interconnection date shifts the entire credit to the next tax year.

SolarInfoPath has reviewed financial models across multiple commercial solar markets. The projected credit and the realized credit often do not match because the sales process does not explain which conditions drive the final number.

Official IRS Sources Give You the Facts Your Installer Does Not

IRS guidance on Form 3468 and Section 48 is publicly available on IRS.gov. The official federal resource for clean energy tax credit policy is also available through energy.gov’s clean energy tax credit resources. Reading your installer’s credit projection alongside these official sources gives you a second check before you commit.

Frequently Asked Questions

What is the IRS Section 48 energy credit?

Section 48 is a federal business tax credit that cuts your federal tax bill dollar for dollar by 30% of the cost of a qualifying commercial solar system placed in service in 2026. The 30% rate requires prevailing wage compliance. Without it, the rate is 6%.

What does Section 48 cover for solar?

Section 48 covers solar panels, inverters, mounting hardware, wiring, installation labor, and battery storage connected to the solar array. It does not cover roof replacements, structural work, or electrical panel upgrades for the building.

Who qualifies for the Section 48 tax credit?

Businesses and commercial property owners who own a qualifying solar system placed in service during the tax year. Lease and PPA customers do not qualify because they do not own the system. Homeowners use Section 25D instead of Section 48.

How does ITC work for solar?

The ITC reduces your federal tax bill dollar for dollar in the year your solar system is placed in service. If the credit is larger than your tax bill, the unused portion carries back one year or forward up to 20 years under Section 39.

How much ITC can you claim?

The base rate is 30% with prevailing wage and apprenticeship compliance. An Energy Community Bonus adds 10%. A Domestic Content Bonus adds 10%. A Low Income Community Bonus adds 10% to 20%. Without prevailing wage compliance, the rate drops to 6%.

What systems qualify for ITC?

Commercial solar PV systems, battery storage under Section 48(c)(6), fuel cells, small wind turbines, and combined heat and power systems. Section 48E uses an emissions-based test for projects starting construction after December 31, 2024.

What is the difference between Section 48 and Section 48E?

Section 48 uses a fixed list of approved technologies. Section 48E applies to projects starting construction after December 31, 2024, and uses a greenhouse gas emissions test. Credit rates are similar, but documentation requirements differ.

How do businesses claim solar ITC?

File Form 3468 to calculate the credit and Form 3800 to apply it against your federal tax bill. Partnerships and S corporations pass the credit to owners through Schedule K-1.

What is the solar tax credit percentage in 2026?

30% for systems meeting prevailing wage and apprenticeship rules. 6% for systems that do not meet those rules. Bonus credits can bring the total rate to 40% or more in qualifying areas.

Can energy storage qualify for ITC?

Yes. Standalone battery storage qualifies as energy storage technology under IRC Section 48(c)(6). Battery storage placed near or connected to the solar array also qualifies as part of the solar property ITC basis.

What are the ITC carry-forward rules?

Unused ITC carries back one year by amended return or forward up to 20 years against future tax bills under Section 39 of the Internal Revenue Code.

What documentation is required for the solar tax credit?

You need an itemized installer invoice, a utility permission to operate letter or interconnection approval, and certified payroll records showing Davis-Bacon prevailing wage compliance. Bonus credit claims require location or content verification documents.

This article by SolarInfoPath (2026 research framework) is part of a comprehensive solar knowledge architecture covering all major high-value sectors including legal disputes (installation negligence, contracts, liability, fraud, lawsuits, liens, HOA and permitting disputes), financial structures (loans, PPA/lease agreements, DSCR financing, tax equity, investment and project finance), tax law (ITC, Section 48/25D, MACRS depreciation, bonus credits, IRS audits, recapture rules, domestic content and IRA/OBBBA compliance), insurance and risk (property damage, hail/wind/fire claims, bad faith insurance disputes, warranty coverage), policy and regulation (net metering, FERC interconnection, state utility rules, incentive programs and regulatory changes), commercial and utility-scale development (EPC contracts, construction delays, performance bonds, receivership, bankruptcy, asset sale and restructuring), real estate impacts (home value, solar leases, liens, title issues, HOA restrictions, easements), and emerging market structures such as battery storage, community solar, agrivoltaics, SRECs, yieldcos, and institutional investment funds. All content is based on publicly available regulatory, financial, and legal sources and is intended strictly for educational and informational purposes, not legal, tax, or financial advice. Readers should always verify current laws, utility policies, tax regulations, and contract terms with qualified licensed professionals before making decisions, as solar regulations, incentives, and financial structures frequently change across jurisdictions and time.

Solar Legal Analyst· Policy Researcher· Investigative Finance Writer Lead Analyst & Founder of SolarInfoPath

Morgan Lee is a solar legal analyst, policy researcher, and investigative finance writer with 12+ years of experience in U.S. renewable energy law, IRS tax credit compliance, and solar litigation. He is the founder of SolarInfoPath, a research-driven platform focused on primary-source analysis of solar contracts, tax law, regulatory policy, and industry disputes affecting homeowners and commercial developers.

His work is grounded in original legal and regulatory sources, including IRS notices, FERC and CPUC rulings, state court filings, PACER records, and UCC lien databases. He specializes in solar contract disputes, injury and workers’ compensation claims, PACE financing issues, tax equity structures, ITC recapture rules, MACRS depreciation, and federal and state solar policy frameworks.

Morgan’s analysis spans solar litigation, finance structures, and regulatory developments such as the IRA and OBBBA, interconnection reform, domestic content rules, and battery storage incentives. He also covers EPC contracts, PPAs, project financing, and utility-scale solar investment structures.