In California, a solar lease buyout can cost between $8,000 and $35,000 at closing. Many homeowners find this out for the first time during escrow. If your buyer rejected the lease transfer, or a lender denied your refinance because of a UCC-1 lien, a solar lease buyout attorney in California can review your contract and help you understand your options before the deal falls apart.

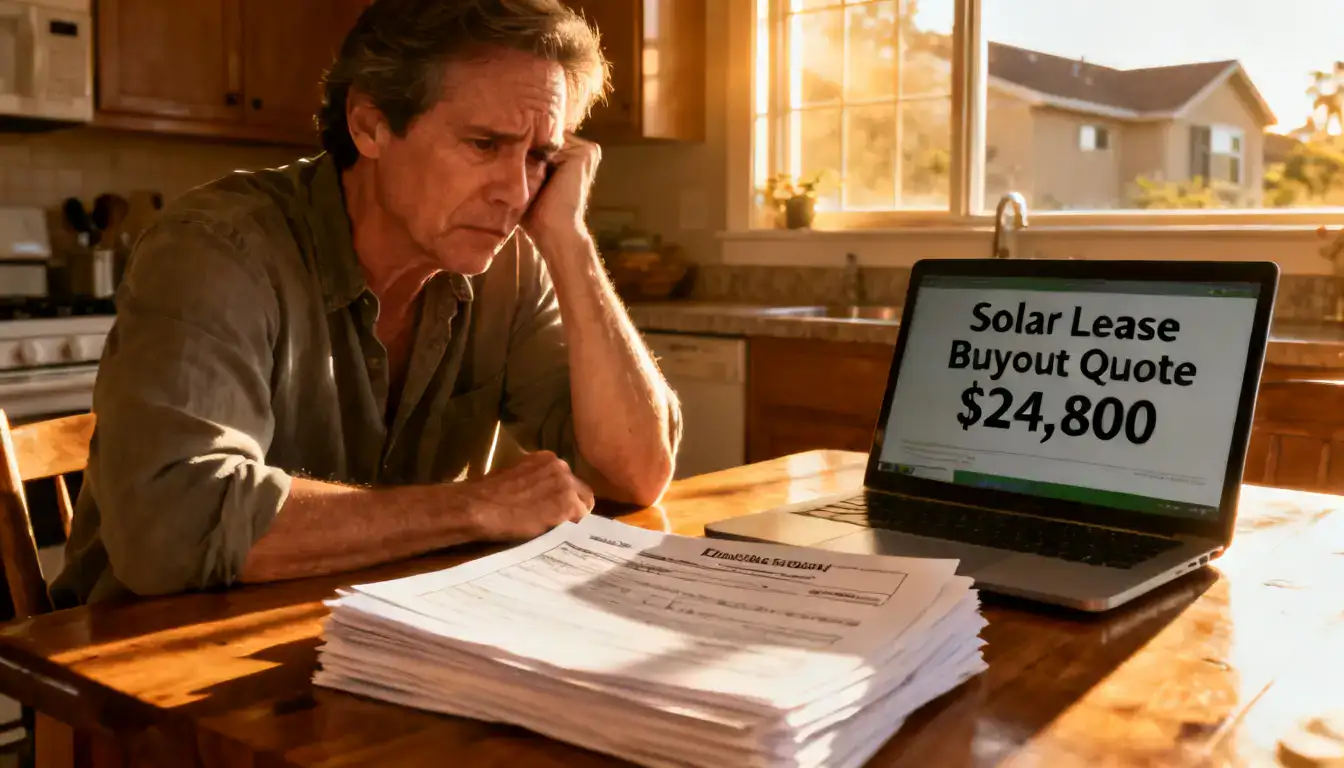

A San Diego homeowner listed her home in early 2026. She had a Sunrun solar lease with 17 years left.

Her buyer wanted the house, but not the lease.

The solar company sent a buyout quote: $24,800.

Nobody mentioned this number during the original lease signing in 2019.

That is the part that shocks most California homeowners. The buyout cost is in the contract. It just never gets explained.

When Do You Need a Solar Lease Buyout Attorney in California?

You need a solar lease buyout attorney in California when a UCC-1 lien blocks your title, a buyer rejects the lease transfer, or a lender denies your refinance because of the solar agreement.

Most homeowners do not realize there is a legal issue until escrow opens. That is usually 30 to 45 days before closing. At that point, the pressure to resolve the lease problem is intense.

Three situations almost always require legal help:

- Your solar company is demanding a full buyout at closing with no room to negotiate

- Your title company flagged a UCC-1 lien and will not clear it without payoff documentation

- Your lender denied your HELOC or refinance application because of the solar lien

Each situation is different. But all three can stop a home sale or refinance in California if they are not handled correctly.

Solar Company Demanding Lease Buyout at Closing: What This Means

When a buyer cannot qualify to assume your solar lease, the solar company can require you to pay off the entire remaining lease value before the sale closes.

This is not a penalty. It is a contract clause. Most California solar leases, including those from Sunrun and Tesla, include a forced buyout provision when lease transfer fails.

The solar company calculates the buyout using the net present value of all future lease payments. That formula often produces a number far higher than homeowners expect.

What surprises most sellers is that this clause is written into the original contract they signed years earlier. It was just never highlighted during the sales process.

Solar Lease Lien on Title: Why Escrow Gets Blocked

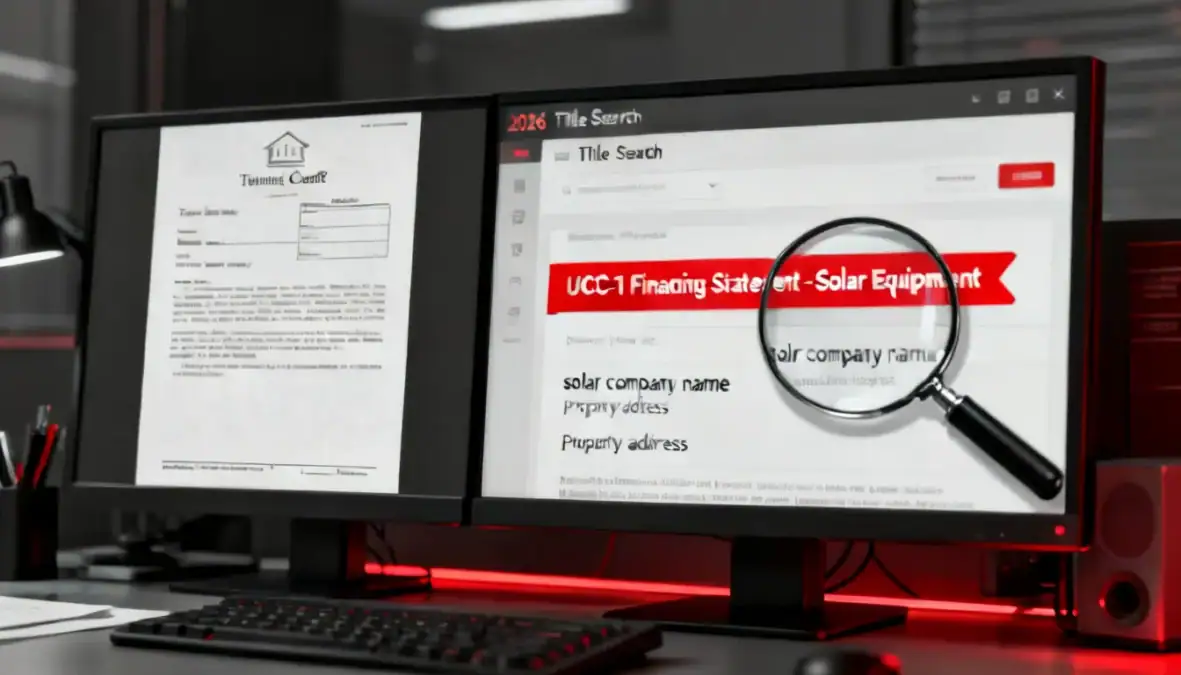

A UCC-1 financing statement filed on your solar equipment creates a recorded interest that shows up during a title search. Title companies cannot clear your title for sale or refinance until that lien is resolved.

A UCC-1 is not a mortgage lien. It does not attach to your land. But it does attach to the solar equipment, which sits on your roof.

In California, title companies treat these filings as secured interests. Before they issue a title insurance policy, they need written confirmation from the solar company that the lien is satisfied or that the lease is being transferred.

If the solar company is slow to respond, this can delay closing by two to six weeks.

HELOC Denied Because of Solar Lease Lien: What Lenders See

California lenders, including those issuing HELOCs and cash-out refinances, often view an active UCC-1 solar lien as a competing claim on your home’s value. This can trigger a denial or a demand for the lien to be subordinated before closing.

Most homeowners applying for a HELOC do not think about their solar lease. The lender’s underwriting software flags it automatically during the title review.

The lender’s concern is straightforward. If they foreclose, they want to know there are no competing interests tied to your home. A solar UCC-1 lien creates that uncertainty, even if the equipment technically stays on the roof.

Getting a lien subordination agreement from the solar company is possible. But it takes time, and some companies refuse to do it without a formal legal request.

How Much Does It Cost to Buy Out a Solar Lease in California?

In California, a solar lease buyout typically costs between $8,000 and $35,000. The exact number depends on how many years are left on the lease, the original monthly payment, and the discount rate the solar company uses in its calculation.

Here is what the numbers actually look like based on 2026 contract patterns in California:

| Lease Stage | Years Remaining | Typical Buyout Range |

| Early stage (years 1–7) | 13–24 years left | $20,000–$35,000 |

| Mid-term (years 8–14) | 6–12 years left | $12,000–$22,000 |

| Late stage (years 15–20) | 1–5 years left | $4,000–$11,000 |

| Final year | Under 12 months | $1,500–$4,000 |

These are California-specific ranges. Rates from PG&E, SCE, and SDG&E, among the highest in the nation at 28 to 31 cents per kWh in 2026, made solar leases very attractive in the 2015–2022 period. Many of those leases are now mid-term, putting buyouts in the $12,000 to $22,000 range.

Why Buyout Quotes Are Higher Than Homeowners Expect

Solar companies calculate buyout costs using net present value, a financial formula that adds up every future payment you would have made and discounts them slightly for time.

The formula is not designed to be simple. It is designed to recover the full value of the lease for the solar company.

Most California leases also include a 2% to 2.9% annual escalator clause. This means your monthly payment goes up every year. When the buyout formula accounts for those rising future payments, the total climbs fast.

A homeowner in Fresno who signed a 25-year Sunrun lease in 2017 at $120 per month, with a 2.5% escalator, would face monthly payments of over $200 by year 17. The buyout at year 8 could easily exceed $18,000 just on the remaining payment value.

This is the part most sellers never see until they are already in escrow.

Projections vs. Reality: What Homeowners Expect vs. What Contracts Show

| Situation | What Sellers Assume | What 2026 Contracts Produce |

| Buyout cost at year 5 | Around $10,000 | $18,000–$26,000 in most California cases |

| Buyout “negotiability” | Flexible and open to discussion | Fixed by contract formula in most cases |

| Lease transfer process | Quick and easy | Requires a buyer credit check and company approval |

| Transfer timeline | A few days | Often, 15–30 business days in California |

| Lender’s reaction to UCC-1 | No problem | Frequent denials and subordination requests |

Can I Sell My House If I Have a Solar Lease in California?

Yes, you can sell your house with a solar lease in California. But the sale requires either a successful lease transfer to the buyer or a full buyout paid at closing. If neither happens, the deal cannot close.

California does not have a law that automatically transfers a solar lease when a home sells. The solar company controls the transfer process, and they decide whether the buyer qualifies.

What Happens to Your Solar Lease When You Sell Your Home

Three things can happen when you sell a home with an active solar lease:

Option 1: Lease transfer to the buyer. The buyer applies to assume your lease. The solar company reviews their credit. If approved, the lease transfers with no cost to you. But the buyer takes on all remaining payments, including the escalator increases.

Option 2: Seller buyout at closing. You pay the full buyout amount from your sale proceeds. The solar company releases the UCC-1. The panels stay. The buyer gets a system with no lease obligation.

Option 3: Prepayment before listing. Some sellers pay off the lease early, before listing, to remove any barrier to sale. This costs the same as a buyout but gives you more time to negotiate.

Can a Buyer Assume a Solar Lease Without the Solar Company’s Consent?

No. In California, a buyer cannot assume a solar lease without written approval from the solar company. Attempting to close without that approval puts both the buyer and seller at legal risk.

The solar company’s approval is not automatic. The buyer must pass a credit review. Some companies use a minimum FICO score threshold, commonly 650 to 700, before approving a transfer.

If the buyer does not qualify, or if the solar company denies the transfer for any reason, you are back to the buyout option.

This is where many California home sales stall in 2026, and where a solar panel property damage attorney familiar with solar contract disputes can help you understand whether the denial was justified under your contract terms.

Solar Lease Early Termination Fee: What California Sellers Miss

Some California solar leases include an early termination fee that is separate from the buyout amount. This fee can add $1,500 to $5,000 on top of the standard buyout calculation.

Not every lease has this clause. But Tesla and some older Sunrun agreements do.

The fee is triggered when the homeowner terminates the lease outside of the approved transfer or buyout process. If you try to cancel the lease rather than buy it out, this clause activates.

Most sellers never look for this clause. A solar lease buyout attorney in California can identify it in your contract before you take any action.

Why Buyers Walk Away From Solar Leases in California

Many California buyers reject solar leases outright when the annual escalator exceeds 2.5% or when more than 15 years remain on the term.

The buyer is taking on a financial obligation that goes with the house. If their electricity rates drop, or if California’s NEM 3.0 policy continues to reduce net metering export credits, the lease payment may eventually exceed the savings from the panels.

California shifted to NEM 3.0 in April 2023. Under NEM 3.0, homeowners with PG&E, SCE, and SDG&E receive significantly lower export credits than under NEM 2.0. A lease that made sense in 2018 may no longer pencil out for a buyer looking at 2026 utility rates.

That financial reality makes buyers cautious, and gives sellers fewer options when a transfer fails.

Solar UCC-1 Lien Removal: Understanding the Hidden Title Issue

A UCC-1 financing statement is filed by the solar company in the California Secretary of State’s office when you sign a solar lease. It creates a recorded security interest in the panels. Until that filing is removed or released, your title is not clear.

This is the part most homeowners never think about when they sign a lease. The panels on your roof are not your property; they belong to the solar company. The UCC-1 protects that ownership interest.

What a UCC-1 Filing Actually Does to Your Property

The UCC-1 does not appear on your county deed. It appears on a separate public record search tied to your name and property address.

But California title companies run both searches before issuing title insurance. When they find the UCC-1, they flag it as an encumbrance that must be resolved before closing.

The solar company must file a UCC-3 termination statement to release the lien. They do this only after receiving full payment of the buyout or a completed lease transfer.

Getting that termination document in time for closing is where delays happen. Some solar companies take 10 to 20 business days to process and file the UCC-3. If your closing date is firm, that timeline creates real pressure.

If you are also dealing with project-level financial disputes, the process used in solar project debt workout situations shows how lien resolution works across different types of solar agreements.

Can a Solar Lease Lien Block Your Mortgage Refinance?

Yes. In California, an active UCC-1 solar lien can cause a lender to pause or deny a mortgage refinance or HELOC application.

The lender is concerned about priority. If you default, they want to know their claim on your property is first in line. A solar UCC-1 creates a competing secured interest, even if it is technically on equipment, not the land.

Some lenders accept a subordination agreement from the solar company. This is a document where the solar company agrees that the lender’s claim takes priority. But not all solar companies offer subordination. And the ones that do often charge a processing fee of $200 to $500 and take 15 to 30 days to respond.

HELOC Denied in California Because of Solar Lease: A 2026 Issue

In 2026, HELOC denials linked to solar UCC-1 filings are increasing in California, particularly in areas served by PG&E and SCE, where solar adoption rates are highest.

What I noticed when reviewing California real estate dispute patterns is that homeowners in Los Angeles and Sacramento are running into this issue more often than those in newer construction areas. Homes installed with leases between 2015 and 2020 are now entering their prime resale years, and the lease complications are hitting all at once.

If your HELOC was denied, the first step is to get the UCC-1 filing number from your title search. Then contact the solar company directly in writing, not by phone, and request either a subordination agreement or a payoff statement.

Sunrun and Tesla Solar Lease Buyout Disputes in California

Sunrun and Tesla are the two largest solar lease providers in California. Both companies have contract structures that frequently create disputes at closing, though for different reasons.

Sunrun Lease Buyout Disputes in California: Common Patterns

Sunrun lease buyouts in California often produce disputes over the timing of the payoff quote and how long the quote remains valid.

Sunrun typically issues a payoff quote that is valid for 30 days. If your closing is delayed, which happens often in California due to interconnection approval timelines and title clearance issues, you may need a new quote. New quotes can be higher if the 30-day window has passed.

Sellers also report disputes over how Sunrun calculates the remaining lease value. The calculation includes future escalator payments, and the discount rate Sunrun applies affects the total significantly.

A solar lease buyout attorney in California can request the full calculation breakdown and challenge the methodology if it does not match the lease terms.

Tesla Solar Roof Lease Buyout: Why These Are More Complex

Tesla solar roof leases are more legally complex than standard panel leases because they combine the roof structure and the solar system into a single hybrid agreement.

A standard Sunrun lease covers panels installed on your existing roof. A Tesla solar roof lease covers a roof that is itself a solar system. This creates a question that most attorneys have not encountered before 2024: What exactly is being bought out, the energy production agreement or the roof itself?

Tesla’s contracts often do not provide a simple buyout formula. Some agreements require a full appraisal of the roof’s energy production value before a buyout can be calculated.

If you have a Tesla solar roof lease and are trying to sell your California home, the timeline for resolving this is longer, often 60 to 90 days, compared to 20 to 40 days for a standard panel lease.

A Contract Clause Most California Homeowners Never Notice

Many California solar leases include a “non-transferability trigger” clause. This activates a forced buyout automatically when the buyer fails the credit review, with no grace period and no appeals process.

This clause is buried in the lease addendum, not the main agreement. It is rarely discussed during the sales process.

When a buyer fails the transfer credit check, this clause activates immediately. The seller then has a set number of days, often 5 to 10 business days, to either pay the buyout or lose the sale.

That is an extremely tight window. Having a solar lease buyout attorney review your contract before you list your home is the only way to know if this clause applies to you.

Solar PPA Transfer Dispute: What New Jersey Cases Teach California Homeowners

California and New Jersey handle solar lease and PPA transfer disputes differently, but both states see the same core problem: buyers who don’t qualify and sellers who are surprised by the cost.

In New Jersey, solar PPAs and leases are governed under different utility frameworks. New Jersey’s utilities, JCP&L, PSE&G, and Atlantic City Electric, process transfer approvals through their own interconnection offices, adding a layer of delay that California does not have.

In California, the transfer approval goes directly through the solar company, not the utility. That means PG&E, SCE, and SDG&E are not involved in the transfer decision. The solar company approves or denies independently.

This makes California transfers theoretically faster. But it also means homeowners have no regulatory body to appeal to if the solar company denies a transfer unfairly. In New Jersey, the utility commission plays a role. In California, your only recourse is legal.

Understanding how solar contracts interact with commercial asset structures is explained in more detail in this guide on commercial solar asset liquidation services, which covers how lease obligations are handled when assets change hands.

Should You Buy Out, Transfer, or Wait?

If you are selling your California home, buy out the lease when the cost is under 3% of your sale price, and the buyer cannot qualify for a transfer. Transfer the lease when the buyer meets the credit threshold and has more than 10 years remaining on a fixed-rate lease.

Here is a simple way to think about it:

Buyout makes sense when:

- The remaining buyout cost is $15,000 or less, and your sale price absorbs it

- Your buyer has a credit score below 680 and is unlikely to pass the transfer review

- You need to close in less than 30 days, and cannot wait for a transfer approval

Transfer makes sense when:

- Your buyer has strong credit (680+) and is willing to take on the lease

- The escalator rate is 2% or lower, making the lease financially attractive

- The remaining term is under 12 years

Delay the sale when:

- The buyout quote exceeds 5% of your sale price, and you have time to negotiate

- The solar company has not responded to your transfer request within 15 business days

- You are pursuing a subordination agreement for a refinance and want to avoid closing pressure

If Your Buyer Refuses the Solar Lease

When a buyer refuses the lease, not because they don’t qualify, but because they don’t want it, you have two choices: buy it out from your sale proceeds or reduce your asking price to account for it.

Some buyers use the lease as a negotiating tool. They know the seller is stuck. This is especially common in slower California markets like Fresno and parts of the Sacramento Valley, where buyers have more options.

If you reduce your price, make sure the reduction reflects the actual buyout cost, not a round number. A seller who cuts $20,000 from their price to compensate for a $16,000 buyout is losing $4,000 unnecessarily.

Real Scenarios California Homeowners Are Facing in 2026

Los Angeles Scenario: Buyer Rejected the Lease, Forced $22,000 Buyout

A homeowner in Culver City listed their home at $875,000 in early 2026. They had a 20-year Sunrun lease signed in 2016 with a 2.5% annual escalator. The original monthly payment was $115. By 2026, it had climbed to $148.

The buyer, a first-time buyer with a 660 credit score, failed Sunrun’s transfer credit review. The non-transferability trigger clause activated within 48 hours.

Sunrun issued a buyout quote of $22,400. The seller had 7 business days to respond.

They paid the buyout from the closing proceeds. After commissions, fees, and the lease buyout, their net proceeds dropped by $31,000 from what they had planned.

The seller told their real estate agent: “I didn’t even know I had signed something that said this.”

San Diego Scenario: HELOC Denied Due to Solar Lease Lien

A homeowner in Chula Vista applied for a $60,000 HELOC through their bank in March 2026. Their home was worth $720,000. They had a Tesla solar lease signed in 2020.

The underwriter flagged the UCC-1 lien during the title review. The bank issued a conditional denial; they would proceed only if the solar company provided a subordination agreement.

Tesla’s legal team took 28 days to respond. When they did, they required a $350 processing fee and stated the subordination would expire in 90 days.

The homeowner’s HELOC closed, but three months later than planned. The delay caused them to miss a home renovation project deadline and pay a contractor cancellation fee.

The UCC-1 filing is still active because the lease was not paid off.

Sacramento Scenario: Early Termination Fee Found During Escrow

A homeowner in Elk Grove accepted an offer in January 2026. During the escrow review, their attorney found an early termination clause buried in a 2018 SolarCity (now Tesla) lease addendum.

The clause stated that terminating the lease outside of an approved transfer or buyout process would trigger a fee equal to six months of remaining payments.

With 9 years left on the lease at $140/month, that was an $8,400 additional fee, on top of the standard buyout of $13,200.

The seller had planned to negotiate directly with Tesla to reduce the buyout. That plan would have triggered the termination clause without them realizing it.

Their attorney identified the clause before any action was taken. The seller proceeded with the standard buyout only, saving $8,400 by knowing what was in the contract before making a move.

What to Know Before You Call a Solar Lease Buyout Attorney

The most important thing to do before calling a solar lease buyout attorney in California is to gather three documents: your original solar lease agreement, any lease addenda or amendments, and the most recent UCC-1 filing from the California Secretary of State’s database.

Most attorneys can review these documents in one to two hours. That review tells you three things:

- Whether the buyout formula in your contract matches what the solar company is quoting you

- Whether any early termination fees apply to your specific situation

- Whether you have grounds to challenge the buyout amount

This matters because solar companies sometimes make calculation errors, and homeowners who don’t have legal review accept inflated quotes without knowing they are incorrect.

The IRS also has guidelines that affect how solar lease payments and buyouts are treated from a tax standpoint. If your buyout has tax consequences, reviewing the IRS Section 48 energy credit compliance rules can help you understand whether any credit recapture applies to your situation.

Final Verdict: Solar Lease Buyout in California: When Paying $15,000–$30,000 Becomes the Only Way to Close

For many California homeowners in 2026, paying a solar lease buyout at closing is not optional; it is the only path to a completed sale.

The lease transfer process sounds simple when the solar company explains it at signing. In practice, buyer credit failures, slow company response times, and UCC-1 title complications make it one of the most disruptive parts of a California home sale.

A solar lease buyout attorney in California helps you understand three things before you act: what your contract actually says, whether the buyout quote is calculated correctly, and whether you have any legal options to challenge the amount or the process.

This is not about avoiding the buyout. In most cases, the buyout is the right path. It is about making sure you are not paying more than your contract requires, and that the process does not cost you a sale that should have closed weeks earlier.

If you are also dealing with damage caused during the original installation, separate from the lease buyout issue, the legal steps and documentation process are covered in detail in the solar panel property damage attorney guide.

FAQs: Solar Lease Buyout Attorney California (2026)

Can a solar lease stop a home sale in California?

Yes. If the buyer cannot qualify for a lease transfer and you cannot pay the buyout, the sale cannot close. Most California purchase agreements do not address solar lease disputes, leaving sellers responsible for resolution.

How long does a solar lease buyout take in California?

From request to lien release, most California buyouts take 20 to 40 business days. Tesla solar roof buyouts often take 60 to 90 days. Start the process as soon as you accept an offer.

Can I negotiate a solar lease buyout amount in California?

In most cases, no. The buyout formula is fixed in the contract. However, a solar lease buyout attorney can verify whether the company applied the formula correctly. Calculation errors do happen.

Do all solar leases include UCC-1 liens in California?

Almost all of them do. A UCC-1 is the standard way solar companies protect their equipment. If you signed a lease, not a loan, there is almost certainly a UCC-1 on file with the California Secretary of State.

What happens if the solar company delays my closing in California?

If the delay is caused by the solar company’s failure to issue a payoff statement or UCC-3 termination in time, you may have a claim for breach of contract. A solar lease buyout attorney can issue a formal demand letter to accelerate their response.

What is the difference between a solar lease and a solar PPA in California?

A lease charges a fixed monthly payment for use of the equipment. A PPA charges per kilowatt-hour produced. Both create a UCC-1 lien, and both require a transfer or buyout when you sell. The buyout calculation differs slightly between the two.

This article by SolarInfoPath (2026 research framework) is part of a comprehensive solar knowledge architecture covering all major high-value sectors including legal disputes (installation negligence, contracts, liability, fraud, lawsuits, liens, HOA and permitting disputes), financial structures (loans, PPA/lease agreements, DSCR financing, tax equity, investment and project finance), tax law (ITC, Section 48/25D, MACRS depreciation, bonus credits, IRS audits, recapture rules, domestic content and IRA/OBBBA compliance), insurance and risk (property damage, hail/wind/fire claims, bad faith insurance disputes, warranty coverage), policy and regulation (net metering, FERC interconnection, state utility rules, incentive programs and regulatory changes), commercial and utility-scale development (EPC contracts, construction delays, performance bonds, receivership, bankruptcy, asset sale and restructuring), real estate impacts (home value, solar leases, liens, title issues, HOA restrictions, easements), and emerging market structures such as battery storage, community solar, agrivoltaics, SRECs, yieldcos, and institutional investment funds. All content is based on publicly available regulatory, financial, and legal sources and is intended strictly for educational and informational purposes, not legal, tax, or financial advice. Readers should always verify current laws, utility policies, tax regulations, and contract terms with qualified licensed professionals before making decisions, as solar regulations, incentives, and financial structures frequently change across jurisdictions and time.

Solar Legal Analyst· Policy Researcher· Investigative Finance Writer Lead Analyst & Founder of SolarInfoPath

Morgan Lee is a solar legal analyst, policy researcher, and investigative finance writer with 12+ years of experience in U.S. renewable energy law, IRS tax credit compliance, and solar litigation. He is the founder of SolarInfoPath, a research-driven platform focused on primary-source analysis of solar contracts, tax law, regulatory policy, and industry disputes affecting homeowners and commercial developers.

His work is grounded in original legal and regulatory sources, including IRS notices, FERC and CPUC rulings, state court filings, PACER records, and UCC lien databases. He specializes in solar contract disputes, injury and workers’ compensation claims, PACE financing issues, tax equity structures, ITC recapture rules, MACRS depreciation, and federal and state solar policy frameworks.

Morgan’s analysis spans solar litigation, finance structures, and regulatory developments such as the IRA and OBBBA, interconnection reform, domestic content rules, and battery storage incentives. He also covers EPC contracts, PPAs, project financing, and utility-scale solar investment structures.