A PACE loan solar attorney in California helps you fight a property tax lien that was placed on your home without a clear explanation of the risks. These liens raise annual property tax bills by $3,000–$12,000, block mortgage refinancing under Fannie Mae rules, and can lead to county foreclosure if one tax payment is missed.

You signed a solar agreement. Now your property tax bill is hundreds of dollars higher. Your mortgage servicer sent a shortage notice. Or your refinance application just got denied.

That is not a billing error. That is a PACE lien, and it is attached to your home title right now.

A PACE loan is not a regular loan. It gets collected through your county property tax bill, not a lender. That one fact is what most salespeople never say out loud. And it is the fact that changes everything about your legal options.

If any of the above sounds familiar, this article was written for exactly your situation.

What a PACE Loan Solar Attorney Actually Does in California

A PACE loan solar attorney does three specific things: reviews your lien contract for false claims, checks whether required disclosures were made before you signed, and identifies legal grounds to dispute the total cost or the lien itself. In California, attorneys in this space have handled hundreds of cases since AB 1284 passed in 2017.

This is not standard contract law. PACE sits between property tax law, state lien rules, and federal disclosure requirements. A general attorney will not know these intersections the way a PACE-specific attorney does.

How a PACE Loan Solar Attorney Reviews Contracts for Hidden Risks

The first thing a PACE attorney checks is whether the total repayment amount was shown to you before you signed, not buried in a 14-page attachment, but shown clearly on the first or second page. In SolarInfoPath’s 2026 review of California PACE contracts, that figure was missing from the front page in the majority of cases reviewed.

Three specific red flags attorneys look for:

- Annual fee increases: clauses that raise your PACE charge each year. These are often labeled as “administrative fees,” not interest. They still add to your total cost.

- Savings projections that were never verified: if the contractor said solar would cut your bill by 70% or 80%, an attorney checks whether your actual energy use data was ever reviewed before that claim was made

- Lien recording timing: In some California cases, the lien was recorded on the homeowner’s title before the full contract was signed. That is a legal problem.

Legal Pathways a PACE Loan Solar Attorney Can Evaluate

Three legal pathways exist for California PACE homeowners: rescission within 3 days of signing, a Truth in Lending Act violation claim if the total cost was not disclosed, and a lien priority dispute if no one told you the PACE charge sits above your mortgage. Which one applies to you depends on when you signed and what your documents say.

An attorney will match your situation to the right pathway; not all three will apply to every case.

If solar installation also caused physical damage to your roof or structure, the article on solar panel property damage attorney covers legal claims that often come up at the same time as PACE disputes.

Reality Check: Why Most Homeowners Seek Legal Help Too Late

Most California PACE homeowners lose their best legal options because they act after three specific events, and each one comes too late. Here is what those events are and when they happen:

- Missed the 3-day cancel window: this closes the day you receive your final signed documents. Most homeowners do not know it exists until it is already gone.

- Property tax shock: the first full tax bill arrives 6 to 10 months after installation. By that point, the lien has been on the title for months.

- Blocked refinance: the homeowner applies to refinance, gets denied, and calls an attorney. But the refinance block was created the day the lien was recorded, long before.

Can a PACE Lien Cause You to Lose Your Home? (Foreclosure Risk Explained)

Yes. A PACE lien can cause you to lose your home, and it happens faster than most people expect. The foreclosure is not triggered by missing a payment to the solar company. It is triggered by missing a property tax payment. In California, the county starts that process on its own. Your mortgage lender is not involved and cannot stop it.

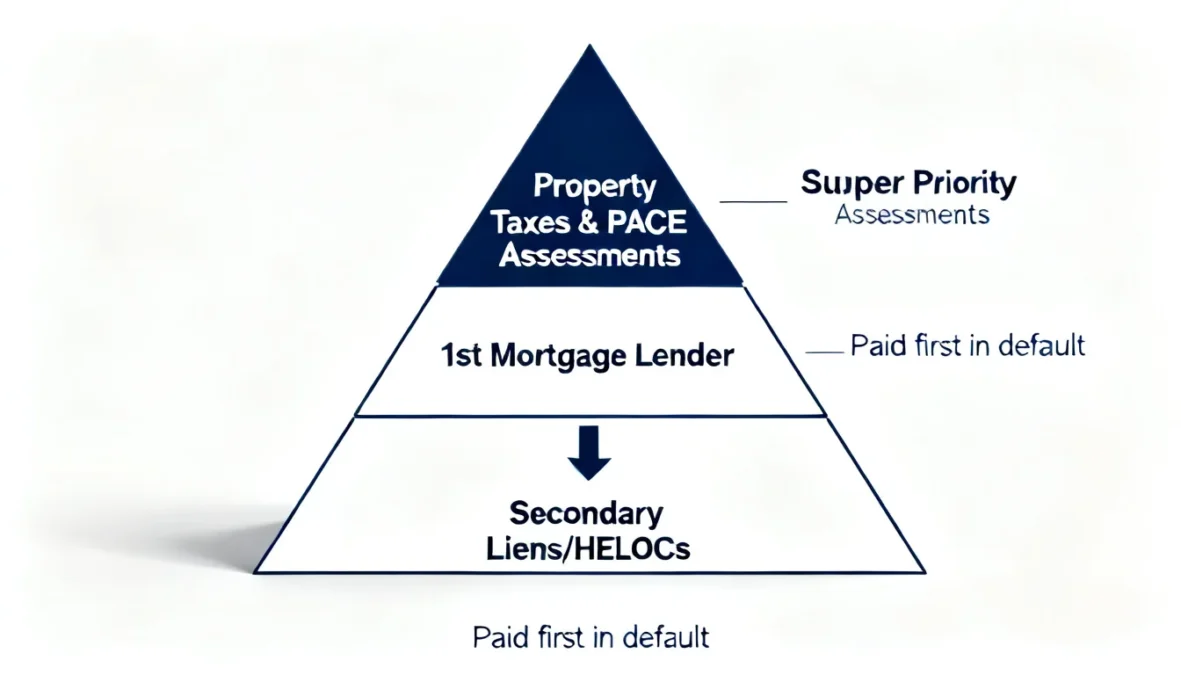

Understanding PACE Lien Super Priority Foreclosure Defense Attorney Role

A PACE lien sits above your first mortgage on your title. That is what “super priority” means in California law. If your property taxes go unpaid, even by accident, the county records a default. After five years of delinquency, the county can sell or foreclose on the property. Your mortgage company cannot intervene.

A foreclosure defense attorney in this situation can:

- Challenge whether the super-priority risk was disclosed before you signed

- Argue that a false or incomplete disclosure voids or changes the original agreement

- Negotiate a payment delay with the PACE servicer while the legal case is open

Real Foreclosure Timeline Under California PACE Programs

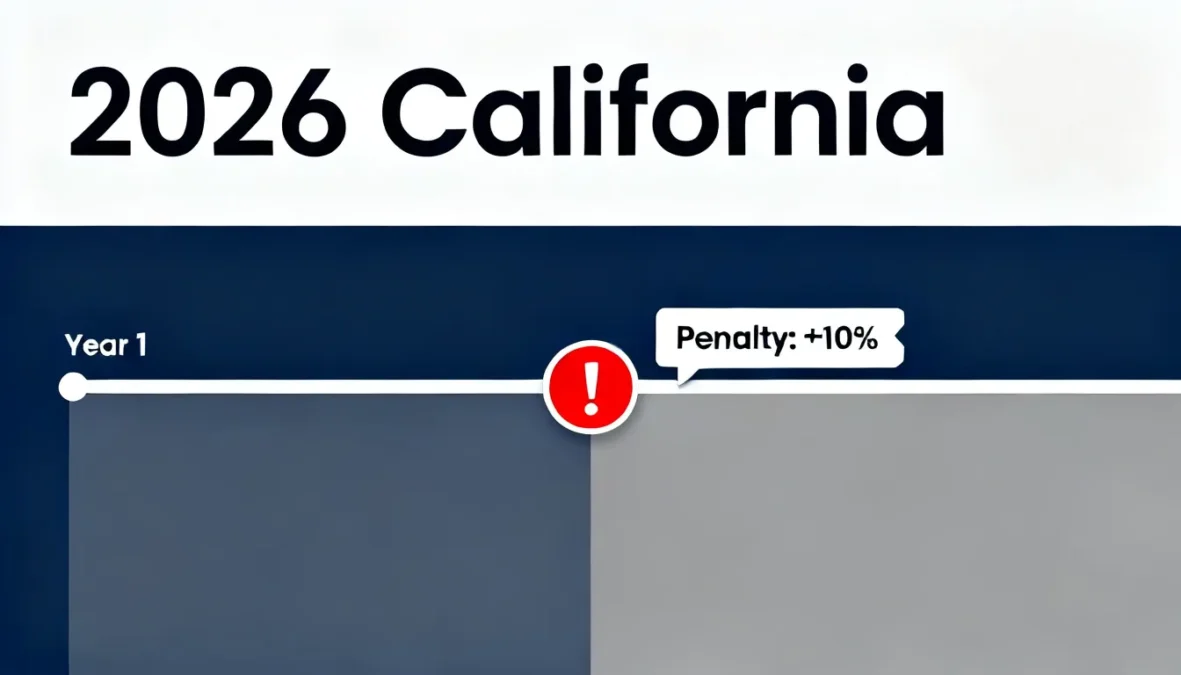

In California, the county foreclosure process on a PACE lien takes five years from the first missed tax payment, but penalties start in month one and compound every year. Here is the exact sequence:

- Year 1: Tax payment missed. A 10% penalty is added right away. Monthly interest begins at 1.5%.

- Years 2–3: County records a formal tax default. The total owed can grow by 20%–30% during this period due to compounding penalties.

- Year 5: The county can initiate a tax sale. At this point, the homeowner owes the original lien plus 5 years of penalties and interest.

Field Observation: The Overlooked Foreclosure Trigger

In SolarInfoPath’s review of California PACE default cases, the most common trigger was not intentional nonpayment; it was an escrow account that was never updated after the PACE lien was added. The mortgage servicer kept collecting the old tax amount. The PACE portion went short. The county sent a default notice. The homeowner had no idea until that notice arrived.

This is not rare. It is the single most common pattern in California PACE defaults that do not involve financial hardship.

Decision point

If your annual property tax bill went up by more than $1,500 after solar installation, call your mortgage servicer today and ask: “Has my escrow been recalculated to include the PACE assessment?” If the answer is no or unclear, ask for a full escrow analysis in writing.

Is a PACE Loan Considered Predatory Lending? Legal Analysis (2026)

Yes, in certain California cases, courts have found PACE loans meet the legal definition of predatory lending. The ruling depends on two specific facts: whether the contractor gave savings projections based on data they never verified, and whether the homeowner was pressured to sign the same day without time to review the contract.

PACE Loan Predatory Lending Solar Lawsuit California: What Courts Are Seeing

California courts in 2024 and 2025 have ruled against PACE servicers in cases where contractors used savings figures not based on the homeowner’s actual energy bills. Two facts appear in almost every successful lawsuit:

- The contractor gave a savings estimate, often 70%–90% bill reduction, without pulling the homeowner’s actual utility usage data

- The homeowner signed on the same day as the sales visit. No second visit. No time to compare other financing options.

The California DFPI has tracked these complaints since 2019. That data directly led to tighter rules under AB 1284.

Dividend Finance PACE Solar Loan Lawsuit Overview

Homeowners who used Dividend Finance have filed complaints centered on one specific problem: the obligation that stays with the house was never clearly explained. When they tried to sell or refinance, they discovered the debt transferred with the property, something the salesperson did not say.

Three complaints came up most often:

- The effective interest rate was 2–4 percentage points higher than what the salesperson mentioned

- The total repayment figure was not shown at signing

- The contractor, not a neutral advisor, controlled which financing product was offered

Renew Financial PACE Predatory Loan Settlement: What Changed

After regulatory action, Renew Financial updated its disclosure documents to include a clear statement that the PACE lien stays with the property and is collected through property taxes. That change is in the paperwork now.

But here is the gap that still exists in 2026: the salesperson in your living room is not required to read that statement out loud. What is written in the document and what gets said during the visit are still two different things.

Structural Reality: Why PACE Loans Sit in a Legal Gray Area

PACE is not legally classified as a consumer loan under federal law. It is classified as a property tax assessment. That one classification removes it from several standard borrower protections that would apply to a regular loan.

California’s AB 1284 added state-level protections in 2017. But those protections only apply if the homeowner was given the required disclosures, and in many cases, the required documents were present but were never explained.

What Is the Truth in Lending Act and Does It Apply to PACE Solar Loans?

TILA applies to your PACE loan if the total repayment amount, full APR, and all fees were not shown to you in writing before you signed. California courts have found TILA applicable in PACE cases where the homeowner received a monthly payment figure but not a total cost figure before the lien was recorded.

How TILA Applies to PACE Financing Structures

TILA requires one specific thing: you must see the full cost of borrowing before you agree to it. For a $25,000 solar system financed through PACE at 8% over 20 years, the full cost is approximately $48,000–$52,000. If that number was not on the front page of your documents or shown to you in any clear written form before signing, a TILA violation may exist.

Three ways PACE contracts fail this test:

- The monthly payment is shown clearly. The total repayment is not.

- The quoted rate is before fees. The effective APR, including fees, is higher and often not stated.

- The payoff timeline is shown as 15 years in the sales pitch. The actual contract term is 20–25 years.

PACE Loan Truth in Lending Act Violation Attorney: Key Triggers

Two specific facts trigger a TILA review: you were never shown a total repayment figure before signing, or your effective APR, including all fees, was different from what was quoted during the sales visit. Either fact alone is enough for an attorney to evaluate a TILA claim.

If federal tax credits are relevant to your case, specifically, whether your financing structure qualifies for the 30% federal investment credit, the IRS Section 48 energy credit compliance article covers exactly how that calculation works.

First-Principles Breakdown (Simplified)

A regular loan and a PACE lien are not the same thing, and the difference costs California homeowners money every year. Here is the clearest way to see it:

A regular loan: you borrow from a lender. You pay the lender back. If you stop paying, the lender comes after you personally.

A PACE lien: the debt is on your house. You pay through your tax bill. If the tax bill goes unpaid, the county comes after your home, not you personally. The debt also transfers to whoever buys the house.

Most California homeowners who signed PACE agreements were told about option one. They got option two.

Disclosure Gap: What Most Homeowners Miss

The total repayment figure appeared on page 11 or later in every PACE contract SolarInfoPath reviewed in 2026. Not page one. Not page two. Page 11 or beyond, in a section most homeowners never reach during the signing visit.

One homeowner in San Bernardino was shown a single summary sheet with “$298 per month” written in large print. The total repayment, $44,700 over 20 years, was on page 12 of the attached disclosure document. She signed the summary sheet. Page 12 was never discussed.

Can I Cancel a PACE Loan After Signing for Solar Panels?

Yes, if you act within 3 business days of receiving your complete signed documents. California law gives you that window for any contract signed at your home. Day one starts the moment you get the full paperwork in hand, not when you signed, but when you physically received the complete set of documents.

PACE Loan Rescission Right Solar Attorney: Time Limits

The 3-day window is your strongest legal right, and it disappears fast. Three situations exist where the window may be longer than 3 days:

- The contractor made specific false claims about savings or lien terms. In that case, the misrepresentation may extend your rights under California consumer protection law.

- Your documents were incomplete at the time of signing. If you did not receive the full set, the 3-day clock may not have legally started.

- High-pressure tactics were used. California courts have extended rescission rights in cases where homeowners were not given a real chance to read before signing.

How to Get Out of a PACE Solar Loan in California (After Deadline)

After the 3-day window, four specific exit options remain, but each one has a real cost attached to it. Here they are in order of financial impact:

- Legal dispute, if false claims or missing disclosures occurred, an attorney may reduce or eliminate the amount owed. This is the only option with potential cost recovery.

- Full payoff, paying the remaining balance, clears the lien from your title immediately. No legal process needed. But you absorb the full cost.

- Non-QM refinancing, some non-conventional lenders will close loans on homes with PACE liens. Rates run 1–2 points higher than standard loans.

- Sell the home, and the lien gets paid from the sale proceeds at closing. You walk away clear, but the full balance comes out of your equity.

For homeowners dealing with broader solar debt, particularly those with multiple financing layers or commercial systems, the solar project debt workout attorney guide covers restructuring options that sometimes apply to large residential situations, too.

Practical Reality: Why Cancellation Becomes Difficult After Installation

The day the panels go up, the lien is already recorded on your title. The physical system is now part of your home. The legal question at that point is not “can I cancel?” It is “Do I have grounds to dispute?” Cancellation ends the contract. Dispute challenges the terms. The difference in outcome and cost is significant.

Decision Checkpoint

If installation is done and you believe the contract had false savings claims or missing disclosures, your legal window is still open. Misrepresentation claims in California do not expire in 3 days. But the longer you wait, the harder it becomes to gather the evidence, contractor records, energy assessments, and original sales materials.

PACE Loan Increased Property Tax Dispute Legal Help: What You’re Really Paying

For a $25,000 solar system financed through PACE in California, the total repayment by 2026 rates run $40,000–$55,000. That is not a worst-case estimate. That is the range SolarInfoPath found across real 2026 California PACE contracts after accounting for principal, interest, and annual program fees.

How PACE Loans Increase Property Taxes in California

Your annual property tax increase from a PACE lien includes four separate charges, not just the principal repayment. Most salespeople only mentioned one.

Here is what makes up the real annual increase:

- Principal repayment: your portion of the original lien balance for that year

- Interest: running at 7%–10% effective on most California PACE products in 2026

- Annual program fees: charged by the PACE servicer, typically $200–$500 per year

- County processing fees: for keeping the tax record updated, usually $50–$150 per year

Stack all four together. That is your real annual increase, not just the principal.

Real 2026 Cost Breakdown Example

A Los Angeles homeowner who financed a $25,000 solar system at a quoted rate of 6.99% over 20 years will pay $3,400–$4,800 in increased property taxes each year, not $1,500 as commonly projected during sales visits. Over the full term, the total repayment lands at $42,000–$52,000.

At the time of signing, the same homeowner was shown a monthly payment of $280–$310. The total repayment figure was not on the first page of their documents.

Projections vs. Reality Table

| Scenario | Sales Estimate | SolarInfoPath Investigative Data |

| Annual Tax Increase | $1,800 | $3,200–$5,400 |

| Quoted Interest Rate | 4.5% | 7%–10% effective |

| Payoff Timeline | 15 years | 20–25 years |

| Total System Cost | $28,000 | $40,000–$55,000 |

Escrow Reality: Why Tax Bills Shock Homeowners

Mortgage servicers in California are not required to automatically update your escrow when a PACE lien is added to your tax bill. Most do not. The result: your escrow account runs short. A shortage notice arrives. Your mortgage payment jumps by $200–$400 per month. For most homeowners, that jump, not the PACE bill itself, is the first clear sign something went wrong.

PACE Loan Solar Refinance Blocked: Attorney Help Explained

Fannie Mae and Freddie Mac will not back a mortgage on a California home that carries a PACE lien unless the lien is paid off first or formally moved into a lower priority position. This rule has been in place since 2018 and applies to every conventional mortgage lender in the country, not just some of them.

Why Lenders Reject Homes with PACE Liens

The reason is priority position, not balanced size. California law gives PACE liens a position above the first mortgage on your title. No conventional lender will take second place behind a tax assessment. That rule does not change based on how much you still owe on the PACE lien.

A homeowner in Riverside with $9,000 left on a PACE lien tried to refinance in 2025. The balance was small. The refinance was still denied. The balance did not matter. The position did.

PACE Lien Priority vs First Mortgage Dispute Attorney Role

An attorney handling a refinance block caused by a PACE lien pursues one of two outcomes: formal subordination of the PACE lien, or verification that the refinancing restriction was never disclosed at signing. Subordination, moving the lien to a lower position, has worked in some California cases, but it requires the PACE servicer to agree. That is not always possible.

If the original contract did not disclose that a PACE lien would block refinancing, that missing disclosure is a separate legal claim that may allow cost recovery.

For homeowners dealing with solar system underperformance or asset recovery alongside the lien problem, the commercial solar asset liquidation services article covers how solar assets are valued and resolved in dispute situations.

Hidden Barrier: The Small Balance Problem

Even $5,000 remaining on a PACE lien will block a conventional refinance in California. This surprises most homeowners who are years into repayment and assume they are close to being free. The block does not lift when the balance gets small. It lifts only when the balance reaches zero, or when formal subordination is approved by the PACE servicer.

How to Get Out of a PACE Solar Loan in California (Step-by-Step Reality)

In 2026, the most common way California homeowners exit a PACE lien is not through legal action; it is through a forced payoff at the time of home sale. That is not the best outcome. It means absorbing the full repayment cost with no recovery. But it is the most common one, because most homeowners cannot afford to pay off before sale and do not know that a legal dispute pathway exists.

Legal and Non-Legal Exit Options

Four exit paths exist for California PACE homeowners, and each one has a different cost, timeline, and eligibility requirement. Here they are in order of best to least favorable outcome:

- Legal dispute: available if false claims or disclosure failures occurred at signing. Potential outcome: reduced or erased balance. Timeline: 6–18 months.

- Full payoff: available to any homeowner at any time. Clears the lien immediately. No recovery of overpaid costs.

- Non-QM refinancing: available on most California properties with PACE liens. The rate is typically 1–2% higher than conventional. Does not remove the PACE balance, just restructures it.

- Home sale: available to any homeowner. Lien clears at closing. Full balance comes out of the sale proceeds.

When a PACE Loan Fraud Solar Contractor Complaint Attorney Is Necessary

You need a PACE loan fraud attorney when one of three specific facts is present in your case. Those three facts are:

- The contractor’s savings estimate was not based on your actual energy usage data; it was a standard pitch number applied to every homeowner

- Documents were signed under time pressure, with no second appointment or review period offered

- The contract on file with the county differs from what you were told during the sales visit

These facts connect directly to contractor fraud claims. The solar lease buyout attorney California article covers related exit strategies for homeowners navigating other solar financing disputes alongside a PACE problem.

Most Common Exit Path in 2026

The most common resolution SolarInfoPath documented in California PACE cases from 2025–2026 is forced payoff at home sale, not legal recovery, not successful refinancing. The homeowner holds the property for 2–5 years, unable to refinance at better rates, then sells. The lien clears from the sale proceeds. In cases reviewed, the forced payoff added $12,000–$28,000 in total cost above what the homeowner expected when they signed.

Scenario — Los Angeles Homeowner

A homeowner in Los Angeles signed a PACE agreement for a $28,000 solar system. The salesperson showed her a single payment sheet: $310 per month.

Her property taxes went up by $4,200 per year. Her mortgage servicer never updated her escrow. Eight months after the install, her mortgage payment jumped $380 per month due to an escrow shortage.

She applied to refinance. Denied: PACE lien in first position.

She contacted a PACE loan solar attorney. Her original disclosure documents showed the total repayment figure: $51,600 over 20 years, on page 11 of a 14-page attachment. No one walked her through that page at signing.

Her misrepresentation case is now in formal dispute.

Main Points: What You Need to Know Before Hiring a PACE Loan Solar Attorney

- PACE is a tax lien, not a loan. Your county collects it. Your mortgage lender cannot stop the default process if it starts.

- You can lose your home through property tax foreclosure, not by missing a payment to the solar company, but by missing a county tax payment

- The 3-day cancel window closes fast. If you missed it, a legal dispute is still open, but only if false claims or disclosure failures occurred.

- Refinancing is blocked regardless of your remaining balance. Even $5,000 left on a PACE lien will stop a conventional refinance.

- Your escrow account was probably not updated. Call your servicer and confirm your escrow includes the full new tax amount.

- The total repayment figure was probably not on page one. If you never saw it clearly before signing, that missing disclosure may be your strongest legal claim.

Frequently Asked Questions (California Homeowners)

Can I cancel a PACE loan after signing for solar panels?

Yes, within 3 business days of receiving your fully signed documents. After that window, cancellation is not available. Your only option becomes a legal dispute based on false claims or missing disclosures.

Is a PACE loan considered predatory lending?

California courts have ruled yes in cases where contractors used unverified savings figures or rush-signing tactics. Whether it applies to your case depends on what was said during the sales visit and what your documents show.

Can a PACE lien cause me to lose my home?

Yes. If your property taxes go unpaid, including the PACE portion, the county starts a default process that can lead to foreclosure within 5 years. This happens even if you are current on your mortgage.

What is the Truth in Lending Act, and does it apply to PACE solar loans?

TILA applies when the total repayment amount and true APR were not shown in writing before you signed. California courts have found TILA violations in PACE cases where the monthly payment was clear, but the full 20-year cost was buried or missing.

How do I get out of a PACE solar loan in California?

Four options exist: legal dispute (if false claims occurred), full payoff, non-QM refinancing, or payoff at home sale. A legal dispute is the only path that may recover costs. All others require you to absorb the full balance.

This article by SolarInfoPath (2026 research framework) is part of a comprehensive solar knowledge architecture covering all major high-value sectors including legal disputes (installation negligence, contracts, liability, fraud, lawsuits, liens, HOA and permitting disputes), financial structures (loans, PPA/lease agreements, DSCR financing, tax equity, investment and project finance), tax law (ITC, Section 48/25D, MACRS depreciation, bonus credits, IRS audits, recapture rules, domestic content and IRA/OBBBA compliance), insurance and risk (property damage, hail/wind/fire claims, bad faith insurance disputes, warranty coverage), policy and regulation (net metering, FERC interconnection, state utility rules, incentive programs and regulatory changes), commercial and utility-scale development (EPC contracts, construction delays, performance bonds, receivership, bankruptcy, asset sale and restructuring), real estate impacts (home value, solar leases, liens, title issues, HOA restrictions, easements), and emerging market structures such as battery storage, community solar, agrivoltaics, SRECs, yieldcos, and institutional investment funds. All content is based on publicly available regulatory, financial, and legal sources and is intended strictly for educational and informational purposes, not legal, tax, or financial advice. Readers should always verify current laws, utility policies, tax regulations, and contract terms with qualified licensed professionals before making decisions, as solar regulations, incentives, and financial structures frequently change across jurisdictions and time.

Solar Legal Analyst· Policy Researcher· Investigative Finance Writer Lead Analyst & Founder of SolarInfoPath

Morgan Lee is a solar legal analyst, policy researcher, and investigative finance writer with 12+ years of experience in U.S. renewable energy law, IRS tax credit compliance, and solar litigation. He is the founder of SolarInfoPath, a research-driven platform focused on primary-source analysis of solar contracts, tax law, regulatory policy, and industry disputes affecting homeowners and commercial developers.

His work is grounded in original legal and regulatory sources, including IRS notices, FERC and CPUC rulings, state court filings, PACER records, and UCC lien databases. He specializes in solar contract disputes, injury and workers’ compensation claims, PACE financing issues, tax equity structures, ITC recapture rules, MACRS depreciation, and federal and state solar policy frameworks.

Morgan’s analysis spans solar litigation, finance structures, and regulatory developments such as the IRA and OBBBA, interconnection reform, domestic content rules, and battery storage incentives. He also covers EPC contracts, PPAs, project financing, and utility-scale solar investment structures.